IN THE MAGISTRATE COURT AT KOTA KINABALU

IN THE STATE OF SABAH, MALAYSIA

CASE NO: 77-20-2007

(Small Claim Procedure)

BETWEEN

OTHMAN BIN

AHMAD ...

PLAINTIFF

AND

TAN SIEW CHOU ...

DEFENDANT

PEMBELAAN KEPADA TUNTUTAN BALAS

1. All the paragraphs of the Defendant's statement of defence are

disputed.

2. Section 29(1) and (2) of the Inland Revenue Board of Malaysia

Act(Act 533) refers only to the board, not to its employees. This statement of

claim is against the employees of the board that has violated the Income Tax

Act as allowed by Section 118 of the Income Tax Act by acting in bad faith and

the Akta Pencegahan Rasuah 1997, Akta 575.

3. Section 21 of the Inland Revenue Board of Malaysia Act(Act 533) does

not protect employees who are not acting in good faith(“for anything which

is done in good faith”). The immunity against legal proceedings is conditional

on good faith.

4. Section 21 of the Inland Revenue Board of Malaysia Act(Act 533) must

be interpreted in full as demonstrated by the judgement “A taxing statute has

to be strictly construed and tax cannot be imposed unless there are clear and

unambiguous words which show an intention to tax a subject: Supreme court

National Land Finance Co-operative Society Ltd. v Director general of Inland

Revenue (1994) 1 MLJ 99”.

5. Section 136 of the Income Tax Act demands that authorization must be

in writing. There is no proof submitted or mentioned by the statement of

Defence of the Defendant that the Director General has approved penalties that

are against the Income Tax Act.

6. Section 118 of Income Tax Act does not exclude action against any

officer including the Director General himself if actions regarding the Income

Tax Act are committed not in good faith.

7. Section 99(1) of the income tax act clearly states that it is not

compulsory for the Plaintiff to appeal to the Special Commissioners as argued

by the defendant in paragraph 4 of the Statement of Defence. Standard of

interpretation of the Income Tax Act must comply with previous court cases as

shown by “Ketua Pengarah Hasil Dalam Negeri v Multipurpose Holdings Bhd. (2002)

1 MLJ 23, KC Vohrah J”.

8. The Plaintiff further argues that the defendant has acted in bad

faith in denying the Plaintiff his right to appeal to the Special Commissioners

despite many letters of objections. No forms were offered for the Plaintiff to

fill in.

9. By misinterpreting the income tax act the way the defendant did in

paragraph 4 of the Statement of Defence, bad faith is further proven. This is

despite the clear directions set by Malaysian courts of law in interpreting the

Income Tax Act so as not to penalise tax payers unnecessarily.

10.

Section 106(3) of the Income Tax Act, only

refers to suits initiated by the Government to recover taxes. The Plaintiff is

currently paying all taxes due including penalties that are disputed. There is

no need for the Government to initiate any recovery suit.

11.

Section 106 clearly shows the need for tax

payers to initiate complaints and any court actions to dispute any tax or

penalties. Otherwise there is no other avenue to rectify other misuses of

powers by the employees of LHDN. The Small claim court is certainly the right

court for tax payers to turn to when the amounts of losses incurred by

government officers who do not act in good faith in interpreting and executing

any statue law. This is contrary to the argument put forward in paragraph 4 and

5 of the Statement of Defence.

12.

Section 21(1) of the Government Proceedings Act

1956, must be interpreted with relevance to the case in hand where the Income

Tax Act, in section 118, and section 21 of the Inland Revenue Board of Malaysia

Act(Act 533), overrides that act. The Plaintiff has no need to take action

against the Government of Malaysia because this case is due to the illegality

and negligence of Government Officers and section 118 reinforces that actions

can be taken against government officers not acting in good faith in executing

the Income Tax Act. There must be reasons why Malaysian Parliament introduces

the phrases “in good faith” in many of the sections of the Income Tax Act, as

preconditions to immunity from prosecution, as argued in paragraph 3 and 4

here.

13.

The Plaintiff can show with proofs that the

Defendant are not acting within the Income Tax Act as shown in my Additional

Arguments In Support of the Statement of Small Claim. Paragraph 7 of the

Statement of Defence is just false declaration.

14.

Paragraph 8 of the Statement of Defence is a

gross misinterpretation of the Income Tax Act by substituting the word “may”

with “have to”. Refer to paragraph 7, 8 and 9.

15.

Paragraph 9 of the Statement of Defence is again

a gross misinterpreting of the Income Tax Act. Refer to paragraph 3 of the

Additional Arguments In Support of the Statement of Small Claim. The imposition

of any penalty is only allowed if no payment were made. Clearly the request by

the Plaintiff and approval of payment by instalments proved that taxes have

already been paid as defined by the Income Tax Act itself in section 103(7)

reinforced by section 108(14) of the Income Tax Act.

16.

Paragraph 9 of the Statement of Defence

sinisterly imply that notices of assessments are the same as notices for

penalties. This is not supported by any law at all. Since there are no

references to the Income Tax Act, this argument must be rejected based on the

standard of interpretation of the case: “A taxing statute has to be strictly

construed and tax cannot be imposed unless there are clear and unambiguous

words which show an intention to tax a subject: Supreme court National Land

Finance Co-operative Society Ltd. v Director general of Inland Revenue (1994) 1

MLJ 99”. Penalties are complete different from assessments. Not many people are

authorised to award penalties. When awarding penalties, there must be

sufficient safeguards and notices

17.

As proven by paragraph 9, of the Statement of

Defence, there are no notices of penalties when they were imposed. Notices of

penalties are vital for complex cases such as the payment of income taxes. The

only statements that the Plaintiff had received keep on showing surplus

payments. These statements are more reliable than the statements mentioned in

paragraph 9 of the Statement of Defence. These are transaction statements where

assessments and payments are clearly stated in full details. In fact the said

“statements of assessments” are just statements of assessments, without any

mention of payments. Failure to provide complete statements where assessments

are weighed against payments, before any penalty is finalised, as demanded by

Section 103(3) and common law of natural justice, is clear proof of acting not

in good faith in executing the Income Tax Act and therefore illegal.

18.

Paragraph 10 of the Statement of Defence is not

the issue raised by the Plaintiff, rather evidence that payments have already

been made. It proves that the Defendant has the authority to collect payment at

any moment. The moment the Defendant has the ability to collect payment,

section 103(3) no longer authorises any officer under the Income Tax Act to

impose penalties.

19.

There is clear proof that penalties were still

imposed, despite official statements prepared by the Defendant clearly showing

penalties being imposed despite excess payments being made by the Plaintiff.

The statement in Argument E/4, paragraph 2 of The Statement of Claim is only

denied but not challenged by the Defendant. This is clear proof that the

penalties were made not in good faith. The rights and privileges conferred by

law are only conditional that they be carried out in good faith.

20.

Evidences that will be easily shown, proves

that actions were taken not in good faith. Even in the Statement of Defence,

misinterpretions of the Income Tax Act exist, as had already been shown in

earlier paragraphs , which provide even more evidences of lack of good faith of

the Defendant. These make a mockery of paragraphs 12 and 13 of the Statement of

Defence.

21.

The court should take note that the Defendant

agree in paragraph 14 of the Statement of Defence, that the excess payments are

not interests, but penalties. Therefore the court must agree that conditions

when imposing penalties must be adhered to in order that justice be carried out

in full.

22.

Paragraph 15 again provides clear evidence that

tax has already been paid via instalments and Section 103 (7) of the Income

Tax Act allows payments of any outstanding taxes via instalments. Therefore

there is no need to impose any penalty any more according to the act. The

Defendant has chosen to ignore this fact and still impose penalties thereby

causing losses to the Plaintiff. The government and the act cannot be faulted,

only the officers who are acting not in good faith and therefore the Defendant

is denied the right and protection under the Income Tax Act and Inland Revenue

Board of Malaysia Act(Act 533) .

23.

Paragraph 16 of the Statement of Defence shows

clearly that the Plaintiff is acting in good faith in trying to pay taxes. The

Plaintiff denies that there has ever been any objections to payment of old

taxes. Only penalties that were imposed on taxes that had already been paid.

Imposing penalties on taxes that had already been paid or considered to be

fully paid by virtue of the Plaintiff's agreements and requests for payment

via instalments.

24.

The Plaintiff's willingness to pay via

instalments, admitted by the Defendant, is not interpreted as a good faith in

attempting to pay any tax as indicated by the Defendant in Paragraph 17. This

is further proof that the Defendant is not acting in good faith in dealing

with the Plaintiff.

25.

Paragraph 18 is claimed without any reference

to any section of any act relevant to this case. The Plaintiff has proof that

the practise of making PCB deductions only for “the relevant current year only”

is against the law. Firstly, there is no such phrase in the act. In fact, the

only available section is in the Income Tax (Deduction From Remuneration)

Rules, Rule 10 (1), the phrase “total amount of tax deducted” shows clearly

that those salary deductions are taxes that are being paid. Since there is no

additional words such as current year, the deduction must be interpreted as

what it should be if natural justice is to be preserved, that is, it is the

payment of any tax, not future taxes, because future estimates are not taxes

yet.

26.

By using common sense, guided by the Income Tax

Act, it should be clear that taxes are only incurred once they are properly

assessed. The assessments are not made at the current year. For example, the

assessments for the current year 2006, were only made on the 30th of

April, 2007. The deductions of salaries under the Income Tax (Deduction From

Remuneration) Rules, Rule 10 (1) are provided for citizens to pay taxes. If

there are no tax, payable, the money should be automatically be used to pay any

tax that may appear, as stipulated by the Income Tax Act. If none, it can be

used as reserve.

27.

Paragraphs 20 to 25 have already been argued in

previous paragraphs here.

28.

None of the paragraphs in the Statement of

Defence have shown any remorse or complete defence against all allegations. The

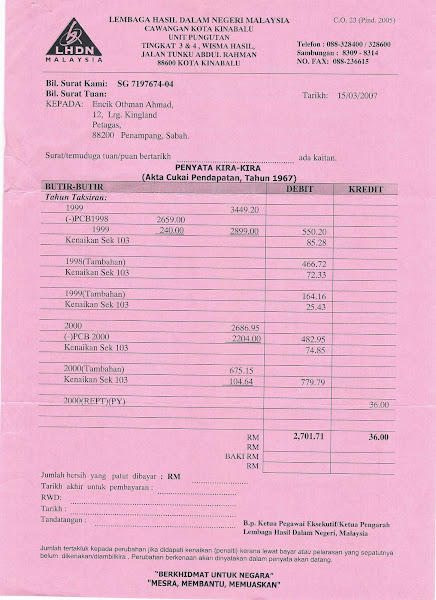

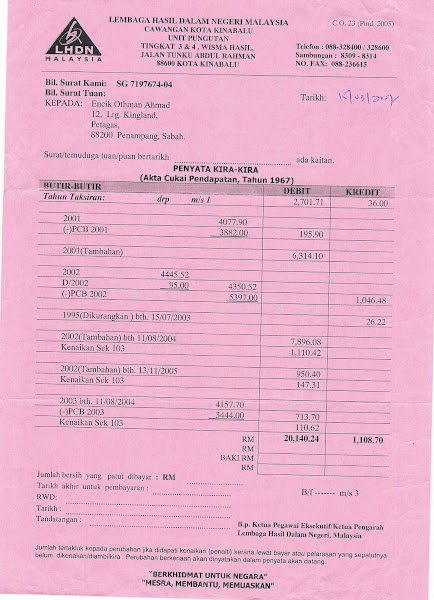

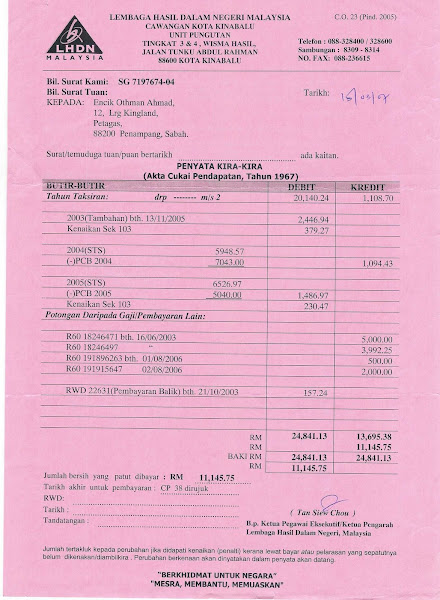

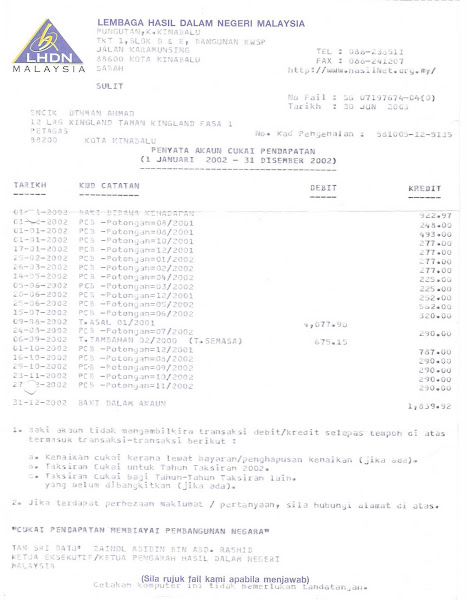

Defendant has not bothered to defend why there are discrepancies in the figures

in the Co23 documents with the Computerised Transaction documents which are the

most important point for the Plaintiff in proving that the Defendant is acting

not in good faith. In fact it is illegal to falsify official documents. By not

defending against an illegal act, it shows that the Defendant is guilty as

charged.

29.

All the statements of defences in the Statement

of Defence have been shown to be false. In fact, they provide further evidences

to prove beyond reasonable doubt that the Defendant is acting not in good faith

in imposing penalties because taxes have already been paid as acknowledged by

the Income Tax Act through instalments.

30.

Furthermore, there is no defence offered against

the discrepancies between the official statements i.e. the Co23 documents(acting

as invoices) versus the actual computerised transaction records(acting as

receipts). Even the Director General of Inland Revenue admitted in newspapers

that LHDN has problems with record keeping. The Defendant's failure to double

check any of the Plaintiff's consistent objections and calculations, shows that

the Defendant is acting not in good faith and therefore does not deserve to be

protected. The acts relevant to this case, mentioned previously clearly shows

that immunity can only be granted with conditions that actions be made in good

faith.

31.

The claim by that the Defendant is only acting

on the instructions of higher authorities must be dismissed because there is no

single evidence or argument offered. Ignorance is not a defence.

32.

The violations of the Statute Laws by the

Defendant give ground for the Small Claim by the Plaintiff as supported by the

“Akta Tafsiran(Akta 388)”, section 58 and 121, where it is stated that

“pengenaan penalti tidak menghalang kepada tindakan sivil”

33.

“Akta Tafsiran(Akta 388)”, section 62A, allows

the admission of electronic media as evidence provided the data can be

verified. The Defendant has failed to challenge the source of evidence as

stated in the Statement of Claim by the Plaintiff in Paragraph 3.

34.

“Akta Tafsiran(Akta 388)”, section 13 shows that

Statue Laws are public unless they are clearly stated. The Plaintiff can use

relevant acts in getting judgement of claims against damages.

35.

In “Akta Pencegahan Rasuah(Akta 575)”, section

2,”Tafsiran, “suapan” ertinya – (d) apa-apa jenis balasan berharga , apa-apa

diskaun, komisen, rebat, bonus, potongan atau peratusan”. Since the employer of

the Defendant, gives out bonuses and other valuable incentives for success in

collecting taxes, this can be regarded as corruption, when the taxes are

collected illegally.

36.

In “Akta Pencegahan Rasuah(Akta 575)”, section

12, “Penerimaan atau pemberi suapan adalah bersalah walaupun maksud tidak

terlaksana atau perkara tidak ada hubungan dengan hal-ehwal atau perniagaan

prinsipal”, which supports the corruption charge despite the uncertainly of

getting bonuses or other financial incentives from the employer of the

Defendant, i.e. LHDN.

37.

In “Akta Pencegahan Rasuah(Akta 575)”, section

15 (1) “Mana-mana pegawai badan awam yang menggunakan jawatan atau kedudukan

untuk mendapat apa-apa suapan adalah melalukan suatu kesalahan”, frofm the

Statement of Defence, the Defendant of being treated as a government servant so

is bound by this act if it is proven that the Defendant has misused any

authority. No monetary exchange need to occur as had been proven by the

corruption charge against Anwar Ibrahim versus the Malaysian Government.

38.

In “Akta Pencegahan Rasuah(Akta 575)”, section

15 (2) “.mengenai pegawai itu, atau mana-mana saudara atau sekutunya, mempunyai

kepentingan, sama ada secara langsung atau tidak langsung”. This section gives

the burden of proof to the Defendant. In secion 2, “sekutu bererti – (c)

mana-mana firma yang orang itu, atau mana-mana penamanya, menjadi pekongsinya

atau”. The employer of the Defendant, LHDN, can be considered as its partner

because of the way the emoluments were given out. Failure of the Defendant to

challenge Paragraph 3 and 4 of the Statement of Small Claim, makes the

Defendant guilty as charged because there is not sufficient proof given that

the Defendant is not guilty as charged in the Statement of Small Claim.

Ignorance that these are not within the jurisdictiion of Act 575, cannot be

used as a defence.

39.

In “Akta Pencegahan Rasuah(Akta 575)”, section

19 , “Pembuatan pernyataan yang palsu atau mengelirukan, dsb. kepada pegawai

Badan atau Pendakwa Raya, (3) “Bagi mengelakkan keraguan, adalah diisytiharkan

bahawa maksud perenggan (1)b dan subseksyen (2), apa-apa pernyataan yang

dibuat dalam apa-apa prosiding undang-undang di hadapan mana-mana mahkamah,

...”. In this case, the Statement of Defence is the statement which is

relevant. By not adequately defending against the discrepancies in the Co23

document produced by the Defendant, against computerised transaction records,

the Defendant is guilty of making a false or confusing statement, in the Small

Claims court.

40.

In “Akta Pencegahan Rasuah(Akta 575)”, section

42, reinforces that for charges according to section 15 of Act 575, the burden

of proof lies on the Defendant.

41.

In “Akta Pencegahan Rasuah(Akta 575)”, section

45. “Kebolehterimaan pernyataan orang tertuduh”(4), “... tidaklah menjadi

tidak boleh diterima keterangan semata-mata kerana tiada notis sedemikian

disampaikan kepada orang itu jika notis sedemikian disampaikan padanya dengan

seberapa segera yang semunasabahnya mungkin selepas itu.” The statements made

by the Defendant in the statement of Defence is acceptable despite failure to

provide earlier notice because this current statement can be considered as

such a notice.

42.

In “Akta Pencegahan Rasuah(Akta 575)”, section

45(7) “Tiada apa-apa jua dalam sub seksyen (6) boleh, dalam mana-mana prosiding

jenayah- (a) menjejaskan kebolehterimaan sebagai keterangan perbuatan berdiam

diri atau apa-apa reaksi lain tertuduh semasa apa-apa jua”. This section

supports the impositing of judgement although the Defendant has been silent on

the accusations provided in Paragraph 3 and 4 of the Statement of Small Claim.

43.

In “Akta Pencegahan Rasuah(Akta 575)”, section

49, “Keterangan tentang kelaziman tidak boleh diterima”. The Defendant cannot

claim that the practise of ignoring the discrepancies in the Co23 statements

prepared by the Defendant is a usual practise of the LHDN, is a defence.

44.

In “Akta Pencegahan Rasuah(Akta 575)”, section

50 is irrelevant because this is only a claim of damages as a result of

non-compliance with Act 575. No intention to prosecute the Defendant under the

full legal force of Act 575.

45.

In “Akta Pencegahan Rasuah(Akta 575)”, section

56, “mana-mana pegawai lain yang mempunyai kuasa untuk menyiasat, mendakwa

atgau mengambil apa-apa prosiding berkenaan dengan kesalahan ini”. This gives

the Small Claims Court magistrate to use the provisions of this act in order to

award damages against the Defendant for breaking Act 575.

46.

In “Akta Pencegahan Rasuah(Akta 575)”, section

57, “Mana-mana orang yang tidak mematuhi mana-mana peruntukan Akta ini atau

......., adalah melakukan suatu kesalahan. The Defendant is deemed to be

breaking the law by not complying with Act 575.

47.

The Defendant's failure to act in good faith in

executing the Income Tax Act, and violations of the both the Income Tax Act and

“Akta Pencegahan Rasuah(Akta 575)” resulted in losses that the Plaintiff seeks

to address. The amount stated in the small claims plus costs are therefore

claimed by the Plaintiff.